Click here to sign the People's Proclamation and send it to everyone you know.

Source:Geopolitical Economy

4 US banks crash in 2 months: Banking crisis explained by Michael Hudson

Economist Michael Hudson discusses the collapse of four US banks in two months, giant JP Morgan Chase taking over First Republic Bank, and how government regulators are in bed with the bankers.

Economist Michael Hudson joins Geopolitical Economy Report Ben Norton to discuss the collapse of four US banks in two months, giant JP Morgan Chase taking over First Republic Bank, and how regulators – and the government itself – are in bed with the bankers.

In March, Norton also interviewed Hudson on the collapse of Silicon Valley Bank, Silvergate Bank, and Signature Bank.

Video

Podcast

Transcript

(What follows is a lightly edited transcript.)

BEN NORTON: Hi, everyone. I’m Ben Norton, and this is Geopolitical Economy Report. Today, I have the pleasure of being joined by Michael Hudson, the brilliant economist and author of many books.

Michael is also the co-host of a program here, Geopolitical Economy Hour, which he does every two weeks with friend of the show Radhika Desai.

I had Michael on in March to discuss the collapse of three U.S. banks in just one week – that was Silicon Valley Bank, Signature Bank, and Silvergate Bank.

Yet the crisis has continued since then, and I knew I needed to bring back Michael to talk about the latest developments.

In just two months, four banks in the United States have collapsed. And we now see the latest example this May is First Republic Bank, which is the second-biggest bank in U.S. history to collapse, and which went down and was taken over by JP Morgan.

This is the biggest bank to collapse since 2008, when Washington Mutual collapsed. Although, as Michael has often pointed out, what we should be saying is it was the biggest bank in the U.S. that was “allowed” to collapse, because he pointed out that many banks were actually insolvent, but weren’t allowed to collapse.

Now, First Republic Bank had $207 billion in assets. And there are similarities between this collapse and the previous collapses.

A similarity with First Republic is that the majority of its deposits were uninsured. About 68% of its deposits were above the federally insured limit of $250,000. So that means that there were $120 billion worth of uninsured deposits.

And what’s interesting about First Republic compared to other banks is it had very wealthy clients, and many of them had long-term, low-interest mortgage loans.

So as an example, the CEO of Facebook, Mark Zuckerberg, had a $6 million mortgage with First Republic Bank, and that was at 1% interest.

That’s obviously below inflation, so Bloomberg pointed out that Mark Zuckerberg – a billionaire – was “borrowing for free” for a 30-year mortgage on a mansion.

This is just one example of the kind of clients that were at First Republic Bank.

Now, when I had Michael on last time, he explained how one of the reasons that Silicon Valley Bank collapsed is because it had invested a lot in long-term bonds. And because the Federal Reserve has been aggressively raising interest rates, the value of those bonds has significantly decreased.

So when there was a run on the bank, the bank had to sell those bonds that had lost value and use that to try to pay the depositors. But it didn’t simply have enough, in the end, and it collapsed.

Now, in the case of First Republic Bank, it wasn’t too exposed to bonds like Silicon Valley Bank was, but it did have a lot of long-term mortgages, about $100 billion worth.

So now we see that JP Morgan is taking over First Republic Bank. And JP Morgan has been given a sweetheart deal.

In fact, JP Morgan reported that it expects to make $2.6 billion off of this deal.

As part of the agreement, JP Morgan does not have to pay First Republic Bank’s corporate debt. And the Federal Deposit Insurance Corporation (FDIC), the U.S. government-backed company, has agreed to a loss-sharing agreement.

So because of some of the long-term mortgages that have lost value, if JPMorgan ends up losing some of the value on mortgages and commercial loans, the FDIC agreed to bear 80% of the credit losses.

The very favorable terms of the FDIC loss-share agreement with JP Morgan Chase

Meanwhile, the FDIC is estimating this is going to cost $13 billion to its Deposit Insurance Fund.

That means that, in just two months, since the beginning of March, the FDIC’s Deposit Insurance Fund has paid out around $35 billion to save Silicon Valley Bank, Signature Bank, and now First Republic Bank.

So, Michael, those are the basic facts.

Now, that doesn’t explain what’s happening at a macro scale in the economy, but it does show that it’s another example of how these private banks are getting bailed out by the government, while large banks like JP Morgan, the largest bank in the United States, is given a sweetheart deal, where it’s going to make billions of dollars.

The FDIC is bearing the cost. And this is despite the fact that, as Pam Martens and Russ Martens pointed out at Wall Street on Parade, JP Morgan is actually ranked by regulators as the riskiest bank in the United States.

So giving JP Morgan Chase control over this bank that already had financial issues makes it even riskier for the U.S. financial system.

So I talked about a lot of things there, but those are the basic points.

I want to get your analysis, Michael, and especially in response to the JP Morgan takeover and the increasing concentration of these large banks, the sweetheart deal it got, and the FDIC bailout.

What do you think about all of that?

MICHAEL HUDSON: Well, the entire U.S. banking system is just as insolvent as the banks that you’ve just mentioned.

What’s amazing is that all of this is treated as if somehow it was unforeseeable. And people are saying, like Queen Elizabeth said in 2008, did nobody see this?

Well, I’ve been writing about this, exactly how this would occur for the last 15 years, ever since I wrote [my book] Killing the Host.

And the reason the banks are insolvent now is because of President Obama’s program and his Secretary of the Treasury, Tim Geithner, who appointed the current Federal Reserve President, Powell.

When President Obama decided to bail out the banks, instead of writing down the bank loans to what would have been reasonable levels, instead of saving the junk mortgage victims from their houses, he decided to go along with his boss, Robert Rubin, the former Treasury Secretary under Bill Clinton, and save Citibank and the other big banks that were the most troubled banks of all.

And they’re still the most troubled banks of all, except they have a government guarantee, just like Obama gave them, that no matter how much they lose, they will not lose the money. No matter how much the banks lose in negative net worth, the economy will lose, not the banks.

All of that became implicit when the Federal Reserve decided to help the banks that were insolvent in 2008 and 2009, to help them recover their net worth by quantitative easing.

That is creating $9 trillion worth of Federal Reserve balance sheet support of the banks to enable the banks to drive down interest rates to near zero, 0.1%, which is about what banks were paying their depositors.

And the banks used all of this increasing liquidity. What were they going to do with the [liquidity]?

Well, they lent them out largely to private capital firms. In other words, they lent them out to operators on Wall Street who borrowed from the banks to buy out companies and take them private.

Then they would have the companies borrow money from the banks for billions of dollars of money and pay this money out as special dividends to the private capital companies that had bought them out, leaving companies as bankrupt shells, such as Bed Bath & Beyond.

Well, as long as interest rates were just about zero, you had free credit and you had a debt-fueled stock market boom, the biggest bond market boom in history, and a real estate boom.

All of these things you and I have been discussing for many years now, and I’ve been discussing it on my website and my Patreon group.

What happened then was that the Federal Reserve, under the lawyer, Mr. Powell, he’s not an economist, he’s a lawyer, serving his clients, which are Chase Manhattan, Citibank, and the big banks, to decide, well, there’s a danger of wages rising and we’ve got to keep wages down in order to maintain the profit of the stocks that are fueling the stock market gains.

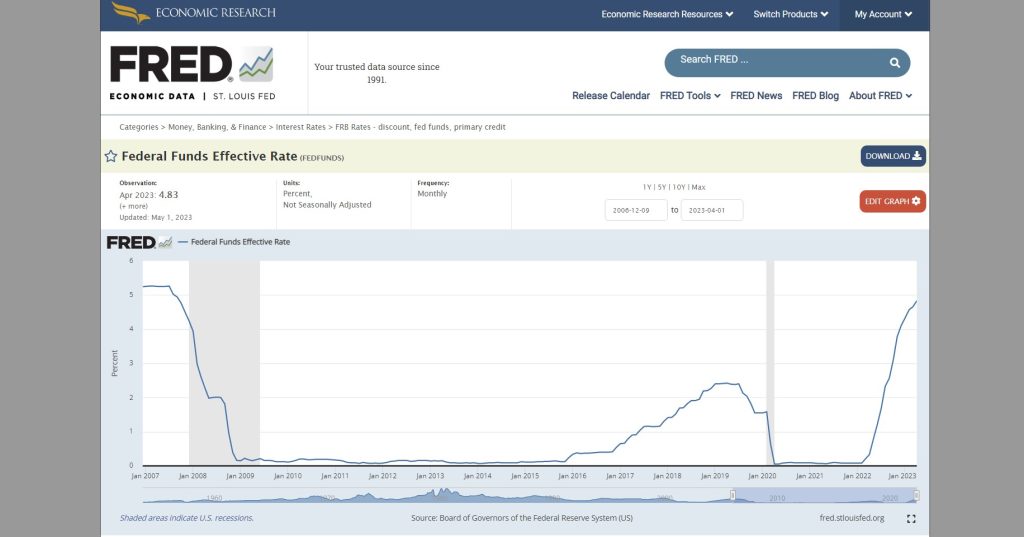

The Federal Reserve decided and announced that it was going to begin raising interest rates from 0% to 4%.

Now, at the time this was publicly announced, I talked to many businessmen, many investors, many CEOs, and every single individual that I knew said, — Oh, they’re going to raise the interest rates. That means that if we hold a long-term government bond, like a 30-year bond, or a 5-year bond, or a 10-year bond, the price is going to go down, because when interest rates go up, the price of bonds go down.

Everyone I knew moved into short-term government bonds, that is, Treasury bills, three-month Treasury bills, or maybe two-year Treasury notes, because they didn’t want to take the loss that occurred if you’re holding a 30-year bond.

And holding a 30-year mortgage is just like holding a 30-year bond. All of a sudden, interest rates are going up, but you’re holding a security, a mortgage or a bond that pays a very low interest rate and whose price has fallen by 30%, maybe even 40%.

Now, that means that if you’re a bank and you have depositors and your assets are reduced in market price by 40%, what are you going to do if your deposits aren’t reduced? You have negative equity.

Well, just about every bank in the country moved into a negative equity position, because all the banks have made fairly long-term loans.

And as the Federal Reserve raised interest rates, that lowered the price of the mortgages that banks held, the Treasury securities that banks held. All of this was going down.

Now, after Silicon Valley Bank went under, for instance, Yves Smith on Naked Capitalism, which is my favorite financial site to follow on these things, said, — Well, Silicon Valley Bank just hopelessly mismanaged their portfolio in holding on to these long-term government bonds. Why did they do it?

Well, here’s why they did it. Imagine what would have happened if Silicon Valley Bank or any bank in America would have acted just like the private individuals who move their personal retirement accounts or their personal financial accounts into short-term treasuries.

They all would have begun to sell their 30-year mortgages or other long-term mortgages. This by itself would have crashed the price of 30-year mortgages.

If they would have sold their 30-year Treasury bonds and said, — Well, we’d better move into short-term treasuries, imagine if all the banks would have decided, we heard what the Federal Reserve said, they’re going to raise the interest rates to 4% and lower the value of these securities by 30 or 40%. Let’s all dump them.

Well, the act of selling them would have caused the prices to decline to a point where indeed, right away, they would have been yielding this 4%. Obviously, there’s very little they could do.

That’s because finance and credit in the United States are privatized.

The crisis that we’re going through today is not the kind of crisis that China would experience because China has made money and credit and banking a public utility.

In the United States, it’s all privatized and part of it is subject to the balance sheet constraints of: What do you do if interest rates go up, the value of your assets goes down, while your liabilities, that is what you owe depositors, continues high?

Well, some of the newspapers said, — Well, why didn’t Silicon Valley Bank and other banks simply take out an option and hedge?

In other words, the suggestion was, — Well, if you know you’re going to have a $100,000 mortgage that’s going to be worth $60,000, why don’t you just get someone to guarantee that in two years or so when the Fed increases interest rates to 4%, you can still go to the counterparty that’s holding the derivative and say, — Okay, now this is only worth $60,000. I want you to pay me $100,000 for it.

Well, how are they going to find a sucker who would have gone into that?

Because the banks that write the derivatives and the futures and the options read the newspapers also and they all read that the Federal Reserve says it’s going to raise the interest rates to 4% and reduce the value of assets to only about 60%.

So they would have said, — Sure, we’ll write it. You’ll have to give us a $100,000 mortgage. That’ll cost you $40,000 for the insurance.

In other words, nobody wants to lose any money. And the fact is, whoever held these long-term securities was going to lose money.

Well, this is exactly what happened to the savings and loan institutions in the 1970s, in the 1980s. There was nothing the banks could do.

The banks were able to survive for a few years despite the fact that the Fed was raising interest rates to 4%.

The banks said, — Well, there’s only one way that we can avoid facing the fact that our assets are much less than our liabilities by just keeping the deposits there. Let’s keep paying the depositors what we were paying all along, 0.2%.

— We hope our depositors are really, really stupid and inertia, and it’s so hard to change a bank account and take money out and buy a government security short term or to buy another financial security. Maybe this inertia will just save us and nobody will do anything.

— But we’ve got to get really stupid people in charge of the Federal Reserve who don’t realize that the banks are insolvent. We’ve got to get flacks, public relations people, for the Fed, like Paul Krugman, who said, — No problem at all. Everything’s going to be okay. Our financial system is great. Nothing to worry about.

And as long as you can get the Fed saying there’s no problem and the newspapers saying interest rates are going up, forget about the fact that when interest rates go up, the price of mortgages and bonds go down.

If you can just ignore that basic balance sheet fact, depositors are just going to be quite happy earning their [0.2%] on their savings account, even though anyone smart has already taken their money out of the bank and invested in government securities that are yielding 4%.

Now, I know many people, friends of mine, who’ve taken their money out of the bank and invested in two-year government notes or short-term money market funds, and they’re getting 4%. Why on earth would they leave the money in the banks?

Well, Silicon Valley Bank and the New York Bank that just went under, went under largely because they cater to the wealthiest depositors, the high-income depositors.

And if you’re a wealthy depositor, you’re smart enough to know that, — Well, when the banks move into negative equity, they can’t cover the deposits. We’d better pull our deposits out now. And instead of making 0.2%, we want to make 4% also. That’s what the Federal Reserve has done for us.

So the Federal Reserve had painted itself into a corner during quantitative easing. By lowering interest rates to just about zero, the Fed has guaranteed that if you ever move out of this position, if you ever go beyond the Obama policy of saving the banks by inflating the capital markets, then you’re going to drive the capital markets bankrupt, insolvent.

So we’re now finally facing the insolvency that Obama and Trump and Biden early on were able to avoid. And it’s just a seventh-grader, well, maybe an eighth-grader, could have done the arithmetic.

Anybody who compares the market price of bank assets to the acquisition price and realizes, well, banks have lost 30 or 40% of their asset values, their deposits are high, anyone doing this is going to say, let’s take our money out of the banks and make a lot more money by buying government two-year notes or ten-year treasuries and lock in these high interest rates now.

And that’s exactly what’s happening. And the newspapers say, — Well, this is such a surprise. Who could have guessed?

And of course they’re moving it into banks like Chase Manhattan or Citibank, which indeed, as Pam Martens said, are serial abusers and violators of regulations.

Of course they’re moving there because the government says, — No bank depositor, no financial investor will lose any money. We promise you that the economy will lose money, not the banks, not the financial sector.

— We promise you that if we have to pay more money to support the financial sector, we’re willing to cut back Social Security. We’re willing to get rid of Medicaid and Medicaid.

— We’re going to get rid of social spending because the economy needs the banks not to lose any money, because that’s, to us politicians, they’re our campaign contributors. They’re who we’re really working for. They’re who we’re protecting. That’s our job as politicians.

And it’s just amazing that nobody is just coming right out and saying this except the few people that are carefully avoided by The New York Times, The Washington Post, and the usual suspects when it comes to saying there’s no problem at all.

So why do they go to Chase?

Because the government has said, — No matter how much money the banks lose, even if Chase and Citibank are insolvent, because after all, they have long-term mortgages, they have long-term loans, they have long-term securities, but no matter what, we’re going to create enough money to bail them out.

Well how much money are we talking about?

Well what has been pushing up all of the prices of the mortgages and the stocks and the government bonds that the banks hold was this $9 trillion in quantitative easing. To make the banks whole from the loss, the government will have to create suddenly another $9 trillion.

The entire economy will not only move into what Mr. Powell calls a recession, but a deep depression, a total financial collapse.

And that’s obviously, it’s almost inconceivable that that can happen, but as long as the government says no bank depositor will lose money, the government will pay. Well, somebody has to lose money, and who do you think it’s going to be, whether it’s the Biden administration or the next Republican administration?

The economy will lose money. This is not only the disaster of Fed mismanagement, because the Fed is managing a financial system that has been privatized and financialized and debt leveraged to the point where it is unsustainable.

And the government and the media are not confronting the fact that the existing debt overhead of the banking system and the financial system and the private capital, that all of this is unsustainable, and we’ve reached the point of unsustainability.

Well, if eighth graders can see that the banks are insolvent, even investors and even some economists can do the mathematics and see how insolvent they are and realize that we’d better take our money and run.

So you’re now having the wealthiest 1% of the country taking their money and running, and that’s what’s causing this problem.

You can expect the wealthiest 1% to contribute very heavily to the 2024 presidential campaign.

BEN NORTON: Very well said. And Michael, I want to emphasize how this highlights regulatory capture.

So you talked about how essentially the so-called regulators are working for the banks.

Now the irony is that, as Wall Street on Parade pointed out, JP Morgan has been rated by regulators to be the riskiest bank in the United States. It’s also the largest bank, and it just swallowed up First Republic Bank.

Now, this also violates antitrust laws. That’s what’s so incredible.

So not only is the US government further empowering and enlarging this risky bank, but antitrust laws say that a financial institution that holds more than 10% of all of the insured deposits in the US cannot expand further and buy up another bank.

Obviously JP Morgan, as the largest bank, has significantly more than 10% of insured deposits in the US. So now it’s growing even further, in violation of the antitrust laws on the books.

And again, I want to highlight this fact, that the FDIC’s deposit insurance fund, according to its filings at the end of 2022, had $128 billion. And in just two months, it’s already spent $35 billion.

So about one quarter of the entire deposit insurance fund to bail out these banks, Silicon Valley Bank, Signature Bank, First Republic Bank. And now we see this crisis spreading further.

So who is watching the watchmen? Who is regulating the regulators? I mean, they’re working for the banks, clearly.

MICHAEL HUDSON: I think you’re missing the point to put the blame on the regulators. The problem’s not that the banks control the regulators and regulatory capture. They’ve captured the government. And it’s the government that appoints the regulators.

So you can’t just blame the regulators, because if the government has been captured by the financial sector, then they’re just going to appoint new regulators who’ve gone to the same business school and have been brainwashed in the same neoliberal “Chicago School” economics that would do exactly the same as the regulators are doing now.

The regulators can only regulate within the existing legal system and the existing political system. They can’t change the political system. And the problem is systemic itself.

The existing financial system cannot survive in the way that it is now structured, because it makes any increase in interest rates drive banks insolvent.

And the government has said, — We’re not going to support the small banks, we’re not going to support the local commercial banks or the smaller revenue banks. They’re not our campaign contributors.

— We know who the campaign contributors are. The Citibank, Chase Manhattan, they’re the big financial firms and the private capital firms.

So the government has basically announced, if you want to keep your money safe, move it to one of the five big systemically important banks. “Systemically important” means, it’s a bank that controls government policy of the financial sector in its own favor.

And you want to be part of a system where the banks [in which] you have your deposits are in control of who gets elected in government to appoint who becomes the Federal Reserve regulator and the various bank agency regulators.

That’s what President Biden says is the key to American democracy. Not realizing the semantic terminological distinction between democracy and oligarchy.

BEN NORTON: Yeah, very well said. And I’ve mentioned, we both have mentioned a few times here, Wall Street on Parade, the amazing financial blog by Pam Martens and Russ Martens.

I highly recommend everyone checking out their website. I’ve invited them on before, but unfortunately they don’t do interviews.

But Michael, they published another article that discussed the $247 trillion in derivatives that 25 U.S. banks are exposed to.

And they speculated that one of the reasons, in March, that these large banks, 11 big banks in the U.S., deposited $30 billion in First Republic Bank to try to save it.

Now, at the time that was portrayed as this great benevolent act by these large banks to try to prevent First Republic Bank from going under.

But Wall Street on Parade speculates that actually one of the reasons they did that was to try to save themselves over their exposure to $247 trillion in derivatives.

And they pointed out that the four big banks that contributed the most to try to save First Republic Bank, the systemically important banks, have 58% of the $247 trillion in derivatives.

So that means that they have over $140 trillion worth of derivatives. I mean, just saying that number sounds just unfathomable. It sounds like we’re talking about imaginary figures.

But what we’re essentially seeing is that the entire U.S. financial system is a big casino. And there are bets that are several times the size of the entire U.S. GDP in the U.S. banking system.

I mean, what’s going to happen with these derivatives?

MICHAEL HUDSON: Well, I describe what has happened before in [my book] Killing the Host. Remember when Greece elected the Syriza party, and it was obvious that Greece could not pay the $50 billion in foreign debt that it had.

And there was a lot of pressure by the incoming government, Varoufakis and others, saying, you’ve got to write down the debts.

And the European Central Bank was all set to write down the debts. The head of the IMF pointed out that the Greek billionaires actually had $50 billion of their own money stashed in Switzerland, of tax avoidance money.

And this $50 billion could have been grabbed by the government and used to repay Greece’s foreign debt.

Well, they were about to write down the debt when President Obama sent his Treasury Secretary, Tim Geithner, over. Obama made a speech, Geithner made a speech. I quote them in Killing The Host.

He said to Europe, — No, no, you can’t let Greece let these bonds go under and default, because the American banks have made such a big bet on derivatives that they would lose money, and you Europeans have to lose the money, not America. That’s how our democracy works.

And so the Europeans said, — Okay, we will make Europe lose money, we’ll make Greece go bankrupt, just so that your American banks, who’ve contributed the most money to Mr. Obama’s presidential campaign, will not have to lose a single penny on their bad derivatives, because now they’re good derivatives because we’ve destroyed the Greek population to help you.

This was probably the most vicious of all of Obama’s actions, apart from the destruction of Libya.

What had happened to Greece under the Syriza government and the bankruptcy is exactly what’s happening on a vastly increased scale today.

The Treasury Secretary’s job is to protect the big banks.

And Ms. Yellen has said, — Just as we’re supporting an unsupportable loser in Ukraine, we’re going to support the unsupportable losers, seemingly, in the American banks.

— We will do whatever it takes so that the big banks do not lose money, even though they’ve made a bad bet, a bet that would have lost all the money, a bet that would have left them insolvent, a bet that would have led them to be taken over by the FDIC and turned from a private bank into a government bank.

— We’re going to prevent that, because that would be socialism. And that’s what we’re fighting against in America, just as we’re fighting against that in Europe.

So you’re having, I won’t characterize what kind of a political system we’re under, but the Treasury Secretary, the Treasury as a whole, has been just as captured by the financial sector as the Federal Reserve.

And you want to look at the Treasury as the bad guys in this. You want to look at the people who are working under Ms. Yellen.

And I think that Pam Martens makes this very clear when she goes through all of the balance sheet maneuverability for this.

When I have a question, I’ve called her to ask for explanations. I mean, you’re right. Her site is the go-to site for this.

So the bottom line is, the whole U.S. economy is being sacrificed to banks that have made bets, and they’ve been bad bets.

Their bets have gone wrong, and they’re bailed out by the Treasury, saying, — Even if you make bad bets, no matter what, we’re going to rescue you, no matter what it takes for the economy at large.

That is the hard iron fist of the financial system controlling the economy as today’s central planner.

BEN NORTON: Yeah, and we now see that this crisis that we’ve seen in the U.S. banking system is spreading, especially to medium-sized banks.

The latest reports show that PacWest is on the verge of collapsing. Also Western Alliance is being targeted and their stocks are falling very rapidly.

And once again, to go back to Wall Street on Parade, they specifically single out short sellers. They say short sellers are targeting these banks because they can see that they could potentially be the next banks to go down.

And they’re trying to make money off of this.

And over at Wall Street on Parade, Pam Martens and Russ Martens argued that the U.S. government is putting its own national security at risk, the stability of the financial system at risk, by not suspending the short selling of federally insured banks.

So what do you think about this argument that short sellers should not be allowed to do this because they’re helping to fuel the collapse of these banks in order to profit from it?

MICHAEL HUDSON: Well, it’s sort of like when they tried to ban betting on horse racing or ban the numbers racket.

The banks can always make, inherently, the equivalent of a short sale. And if they don’t do it in the U.S. economy, they’ll do it offshore in the Cayman Islands. So it is very hard to do something.

The government certainly has the money to hire somebody, a first year BA graduate in business could tell just what the short sellers are saying.

A short term graduate or Pam Martens herself could look at the banks and say, this bank has negative equity, and the government can immediately take it over into the public domain.

But the government won’t do that because they’ll say that’s socialism. And socialism, which we used to call democracy, but now they’ve [renamed] democracy socialism because they think it’s a bad term.

And they say, no, we have to let private enterprise rule. And private enterprise is gambling.

Most banks have not made money, as much money in interest as they’ve made in capital gains. And the biggest capital gains have been derivatives and short sales and options.

So the financial sector isn’t about making loans to industrialists to build factories and employ labor to produce more goods.

It’s made to make loans to gamblers, because that’s where most of the money is made. That’s what the financial system is. And to characterize the system as if it’s part of the economy is the sort of mythology of our time.

The financial system is external to the economy. It’s like a parasite on the economy, using the government as a means of extracting money from the economy or using its own money-creation abilities to make sure that it creates enough money to make sure that the wealthy financial institutions cannot lose.

Smaller financial institutions can lose, but that’s okay to the government, because the big fish eat little fish, and the small banks are taken over by the big banks.

So ultimately the logical result is, if there are only four or five systemically important banks, meaning banks that we’re not going to let go under, and no matter how much they lose, you won’t lose your money in these banks, well, that means, hey, folks, take your money out of your local bank and put it in one of the big banks, because they’re now running things.

That’s the message. And I don’t know why the newspapers and media don’t come right out and say that, or why don’t the banks themselves.

Why doesn’t Chase take out a one-page argument in the New York Times and the Wall Street Journal and say, — Hey, folks, you notice how they bailed us out? We’ll always be bailed out. You’re not going to lose your money here. Put your money in our bank.

That’s a good advertising slogan. Why don’t they think of that?

BEN NORTON: Well, Michael, to conclude here, I just want to give you a quote from [JP Morgan Chase CEO] Jamie Dimon.

He insisted in a media interview that with JP Morgan taking over First Republic Bank, he said, “There may be another smaller one, but this pretty much resolves them all. This part of the crisis is over.”

So, JP Morgan Chase wants us to think that we’ve gone through the worst, that the solution has been pretty much solved. What do you say in response to Jamie Dimon?

MICHAEL HUDSON: Well, all of the banks have suffered the same problem that began with Silicon Valley Bank and the other banks that have gone under.

All of the banks have seen the market price of their mortgage loans and their government securities fall by a large amount, so much that the amount of the decline in their assets has wiped out the equivalent of their net worth.

So they’re in negative equity. They’re technically insolvent, except that the government doesn’t ask the banks to report what is the actual market price of your assets.

That’s a secret. And it’s a secret because if people could see the market price of the assets and what their liabilities, they’d see that their net worth is worse than that of the average homeless person on the New York subways.

And so they just don’t do that.

The fact is that we’re still in the problem that the Federal Reserve painted itself into when it moved to zero interest rates. Any increase in interest rates causes a crash in real estate and bond prices and implicitly stock prices.

And if the government doesn’t bail out the banks, they’re going to be insolvent, like somebody who’s bet the fortune at a racetrack or a casino and has lost their money.

So of course [Dimon] is going to say everything’s okay now.

But what that means is, well, it’ll be okay if the depositors leave their money in the banks and their savings accounts that are paying 0.2% and don’t go to an investment bank or broker and buy government money market funds or Treasury bills.

If they don’t go to Vanguard or one of these companies that’ll set up an account for them to buy Treasury bonds or local government funds, and are willing to give up the money in the banks and let the banks make money off the financial distress, not themselves, then everything will be okay.

But for the bank depositors and for the public to be quiescent, they have to be stupid. And that’s the role of The New York Times and The Washington Post and the other media.

You’ve got to have a financially stupid public. And the best way to do it is to have the university courses teach stupid economics, like that’s what Chicago School is all about, the economic curriculum in the United States.

Don’t look at debt problems. They don’t look at balance sheet problems. None of the problems that are occurring today appear in the economic curriculum that people have to learn in order to see how the economy works.

It’s all a mythology. It’s a fairytale. And you could say it’s sort of the superstition of our time. I won’t dignify it by calling it a religion, even though many banks look like the ancient Greek and Roman temples.

It’s really just a superstition that the financial system works to help the economy instead of, how can we make money from the economy by taking over the government and capturing the whole government, not only the regulators.

BEN NORTON: Well, that’s a good note to end on. I want to thank you, Michael Hudson, an economist and author of many books.

People should go check out his website at michael-hudson.com.

And Michael also co-hosts the show Geopolitical Economy Hour here with Radhika Desai.

I will also link to his previous interview with me, where we talked about the collapse of Silicon Valley Bank, Signature Bank, and Silvergate Bank this March.

Michael, it’s always a real pleasure. Thanks for joining me.

MICHAEL HUDSON: Well, thanks for having me, Ben.

No comments:

Post a Comment